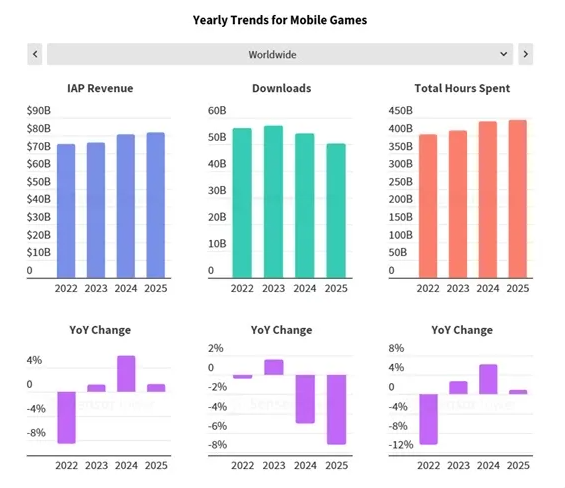

According to the annual Mobile Market Status report published by Sensor Tower, global mobile game applications grew 1.3 per cent over the same period in 2025, to $81.750 billion. The domestic buy-in income from China’s nuclear and leisure games was roughly the same as at $44.68 billion and $32.7 billion, respectively, while the revenue from mixed leisure games increased by 20 per cent to $4.2 billion each year.

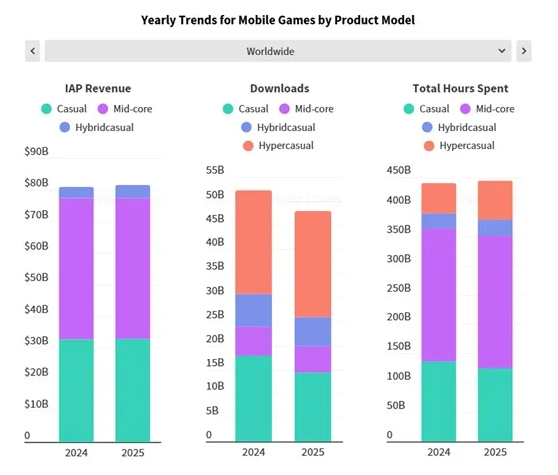

Driven by the success of Last War: Survival and Whiteout Survival, the strategic game achieved the most significant income growth in major global markets in 2025. At the same time, the elitist game has shown strong growth, particularly in Europe and the United States. Global mobile game downloads decreased by 7.2 per cent per year, to a total of 50,411 million in 2025. Of these, the number of downloads of leisure games decreased by 19.5 to 14.35 billion, the number of Central Nuclear Games fell by 10.2 to 5.48 billion, the number of mixed leisure games fell by 10.6 to 6.09 billion, while the number of ultra-recreational games downloads rose by 2.2 per cent to 22.5 billion.

In the three main markets of Asia, North America and Europe, strategic games are the only product that achieves increased downloads. All other products have experienced a decline in downloads in major markets, particularly lifestyle, simulation and intellectual games.

In terms of user participation, total global hand-to-hand use increased by 0.9 per cent over the year, to 44.63 billion hours. Among them, the length of leisure play fell by 8.2 per cent to 12,488 million hours, while the number of middle-nuclear games fell by 0.6 per cent to 22,565 million hours, while the length of mixed leisure games increased by 7.4 per cent to 27,490 million hours, while the length of ultra-recreational games increased by 29.4 per cent to 66,280 million hours. Regionally, the United States and Japan markets, after a decline in 2024, resumed their growth in 2025 and the United Kingdom markets rose. The French market remained stable, while the German and mainland Chinese markets experienced a downturn.

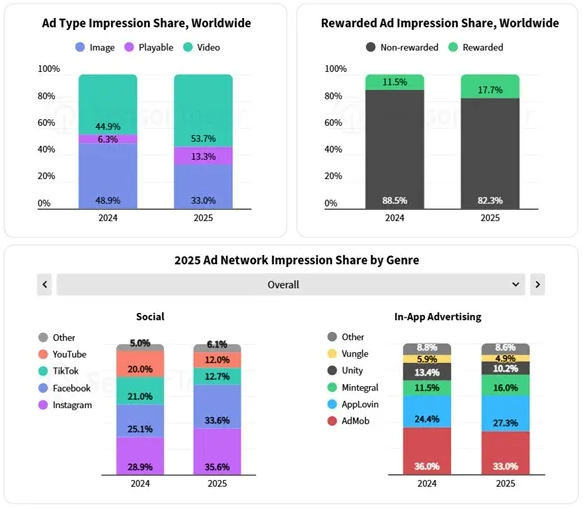

In terms of type of advertising, video advertising dominated by 53.7 per cent of displays in 2025, ahead of photo advertising (33 per cent) and trial advertising (13.3 per cent). The share of stimulating video advertising has continued to increase from 11.5 per cent in 2024 to 17.7 per cent. Instagram is leading 35.6 per cent of the social media advertising network ‘ s share, followed by Facebook (33.6 per cent), TikTok (12.7 per cent) and YouTube (12 per cent). AdMob ranked first in terms of the share of the display of the advertising network in its applications at 33 per cent, followed by AppLovin (27.3 per cent), Mintegral (16 per cent), Unity (10.2 per cent) and Vungle (4.9 per cent).

Related Posts